Knowledge of price changes is a major issue for the commercial property market and for the economy. It is the role of price indices to represent them. Our study shows however that current price indices lead to reward underperforming managers, to underestimate risks and possibly induce inappropriate macro-prudential policies.

Knowledge of price changes is a major issue for the commercial property market and for the economy. It is the role of price indices to represent them.

Indices are used first of all to assess the performance of investment products and their managers. Based on a comparison of the performance (price changes) of investment products with that of the market, these “benchmarking analyses” make it possible to distinguish between underperformers and outperformers; an out-performance will result in additional remuneration for the manager. It should be noted that these analyses are very sensitive because the thresholds for outperformance are narrow: in general, a difference of +1% compared to the market index is sufficient to conclude that there is an outperformance.

Indices are also used by banks to update the value of loans collaterals in statistical-type approaches. Indices therefore influence the amount of required capital to be set aside by banks to manage their risks.

Finally, indices are also the compass that central banks use to guide macro-prudential policies. In this case, the reliability of the indices very directly conditions the relevance of monetary policies and their anti- or pro-cyclical character.

Our analysis suggests that current price indices, which are not adjusted by market judgements on the quality of buildings, are misleading because they result in inadequate representations of price changes.

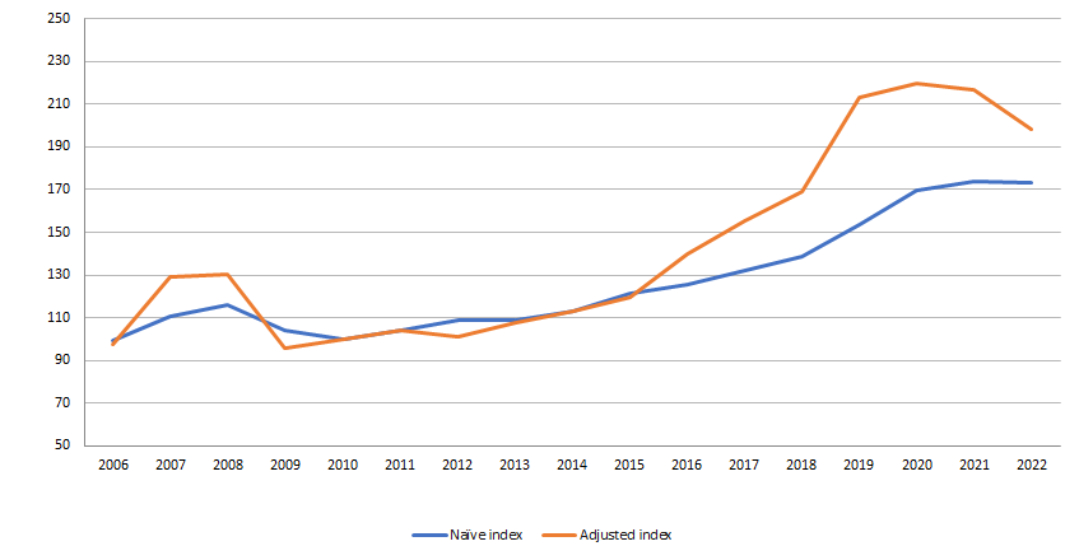

To demonstrate this, we compare the evolution of a price index according to whether it is adjusted by market judgements on quality (“adjusted index”) or not (“naive index”). To do this, we chose office prices in the Ile-de-France region.

The naive index is representative of price indices in circulation. It consists of taking the average or median of prices per unit of floor area for each period and calculating a variation: the variation thus obtained is not only dependent on market changes, but also on variations in the composition of the index between periods. Conversely, the adjusted index consists of analysing price changes for an asset whose perceived quality level has been fixed beforehand. The aim of this construction is therefore to represent a “chemically pure” variation in market prices.

The adjusted index reflects a much higher increase in office prices than the naive index, particularly since 2015. Between 2015 and 2020, i.e. after the start of the central bank’s quantitative easing, the naive index rose by +40%, whereas the adjusted index shows an increase of +80%, i.e. double.

Similarly, from 2020 onwards, while the naive index describes a stabilisation of prices, the adjusted index shows a significant fall, which tends to accelerate between 2021 and 2022.

Price index for offices in Ile-de-France

Why does the adjustment for quality judgements introduce such differences between the indices?

Because buildings are particularly heterogeneous. Thus, apparently stable prices may in fact conceal an increase if the quality of the assets traded has fallen over the period.

This was the case in Paris, for example, after the flight to centrality of the 2009 crisis. Thereafter, between 2010 and 2021, transactions tended to involve assets whose quality continued to decline.

Adjusting the indices for quality judgements is therefore essential. Without it, our study shows that we risk not rewarding good managers, underestimating risks and possibly inducing inappropriate macro-prudential policies

Thus, the credibility of the profession is at stake. The profession must therefore mobilise to produce price indices capable of providing the most adequate representation of market developments.

About Real Quality Rating (RQR)

RQR Global

RQR is the rating agency for the sustainable value of real estate assets. In addition to ratings, RQR provides its clients with sustainable valuation and decision support tools. These tools aim to take sustainable development factors into account and to systematise management processes. RQR is RICS accredited and a member of the International Valuation Standard Council.RQR is the rating agency for the sustainable value of real estate assets. In addition to ratings, RQR provides its clients with sustainable valuation and decision support tools. These tools aim to take sustainable development factors into account and to systematise management processes. RQR is RICS accredited and a member of the International Valuation Standard Council.